[Author Disclosure: This content reflects the views of the author and is provided for informational purposes only. It does not constitute investment advice and is not a recommendation or endorsement by BioTech Funding Portal. Any investment decision should be based solely on the issuer’s official offering materials.]

The Fabry Market Is Bigger Than the Headlines, and the Platform Behind It Is Bigger Still

Every few months a new acquisition reminds the market that lysosomal storage disorders are quietly one of the most durable franchises in rare disease. BioMarin's $4.8B acquisition of Amicus in April 2026 was the latest. So it is worth doing the arithmetic out loud, from primary sources, on exactly how large these markets are and why the platform thesis behind them matters more than any single drug.

Start with Fabry, because the numbers are knowable

You do not need a third-party forecast to size the Fabry market. The approved products are sold by public companies that report their revenue. Add them up:

- Sanofi Fabrazyme: roughly $1.1B in 2024, and still growing double digits (up 12.4% in Q4).

- Takeda Replagal: about $490M to $514M, sold largely outside the US.

- Amicus Galafold: $458.1M, up 18% year over year.

- Chiesi Elfabrio: roughly $20M in early launch.

That is approximately $2.1B in 2024 for a single rare disease. Growth across these franchises has been consistently in the low double digits, doubling roughly every five years.

This puts the 2026 Fabry market comfortably above $2.5B and climbing as diagnosis rates improve and new entrants expand the treated population. When people say the Fabry market is "around $2B," they are describing the floor, not the ceiling.

Gaucher and Pompe each add roughly half again

The same bottom-up method works for the two adjacent lysosomal storage disorders. Sanofi's Cerezyme alone did roughly $800M in Gaucher in 2024; add Takeda's Vpriv and the oral substrate reduction therapies and the Gaucher market lands around $1.5B to $1.8B. Pompe, anchored by Sanofi's Myozyme to Nexviazyme conversion plus newer entrants, sits at roughly $1.3B to $1.5B. Each market is about half the size of Fabry.

Put the three together and you have an addressable enzyme replacement market of about $4B today, growing steadily. Notably, Sanofi by itself generates close to $3B across all three indications, which tells you how concentrated and how valuable this space is to a single strategic owner.

The real story is the platform, not the three diseases

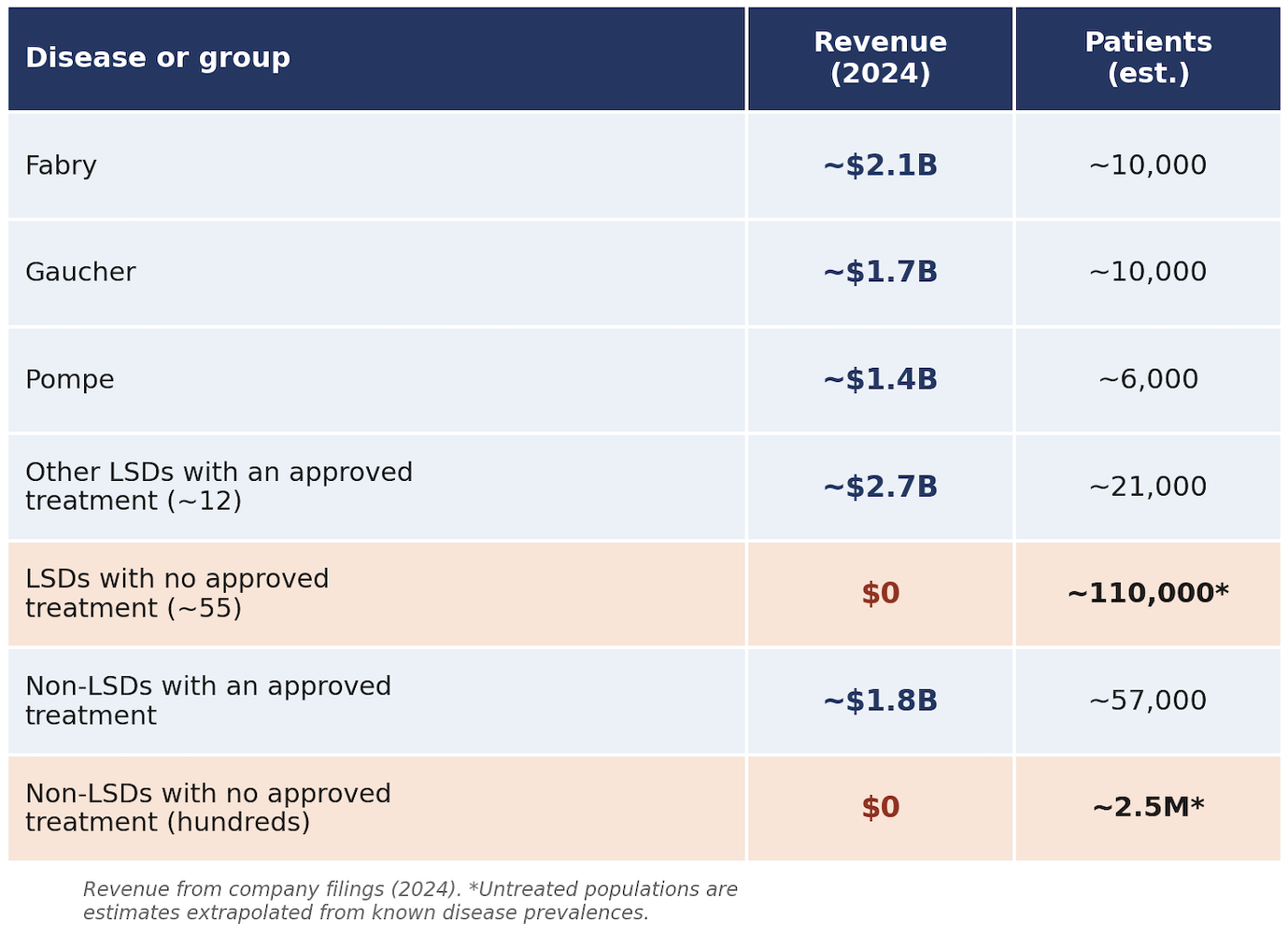

Here is where the framing usually stops too early. Fabry, Gaucher, and Pompe are simply the first three applications of a shared biology: deliver a functional protein from the patient's own cells and correct the defect at its source. The lysosomal storage disorder class alone spans more than 70 distinct diseases, the majority single-gene protein deficiencies. Yet only about 15 of those 70 have any approved therapy today. Roughly 55 do not.

Widen the lens to the full universe of inborn errors of metabolism (the "Non-LSDs"), which the IEMbase knowledgebase catalogs at more than 2,000 disorders, and the treated fraction shrinks to a rounding error. The unmet need is not measured in dozens of diseases. It is measured in hundreds.

How far a platform reaches comes down to one question: delivery

The honest constraint on any cell-based correction platform is which compartments it can reach. There are three mechanisms, and they define three concentric circles of addressability.

The first is cross-correction. Secreted enzyme is taken up through the mannose-6-phosphate pathway into the lysosomes of neighboring cells. This is proven biology. It is the engine behind enzyme replacement therapy and behind our own platform in lysosomal storage disorders. It reaches luminal enzyme deficiencies. Call it the floor.

The second is cell-to-cell protein transfer. In cystinosis, modified blood cells deliver a functional lysosomal membrane transporter to other cells through direct transfer rather than M6P uptake. That alone shows the approach is not limited to soluble enzymes.

The third is cell-penetrating delivery, and it is the one that should make people recalculate.

I initially blogged on it earlier here (https://b2f.bz/sljTY).

It s a paper just out in Cell Reports Medicine showing autologous HSPCs engineered to secrete a cell-penetrating version of frataxin can delay motor symptom onset in a Friedreich's ataxia model.

Frataxin is a mitochondrial matrix protein. It has no lysosome and no M6P pathway and it is not plasma membrane protein rescue. Its cytoplasmic!

The secreted, cell-penetrating payload crossed the plasma membrane, reached the mitochondrion, and rescued function. If that translates, the addressable space is no longer luminal enzyme deficiencies. It is any condition where a functional protein can be fused to a cell-penetrating sequence and delivered by the patient's own circulating cells.

In other words, cross-correction is the floor, not the ceiling. The map the field has been drawing is the smallest of the three circles.

What that means for market size

A $4B enzyme replacement market is addressable today across Fabry, Gaucher, and Pompe, with the same manufacturing process and regulatory pathway.

If you reach for the ceiling, serving every diagnosed and undiagnosed Fabry, Pompe, and Gaucher patient worldwide, roughly 2 million people, at enzyme-replacement-equivalent pricing implies a market north of $500B. That is the horizon. Between the $4B floor and the $500B horizon sit the 55 untreated lysosomal diseases, then the hundreds of untreated metabolic disorders, with the realistic share gated by which delivery mechanism proves out.

That is the optionality, and it is why a platform is worth more than the sum of its first three programs.

Why this matters now

The acquisitions, the rolling BLA filings, and the steady double-digit growth all point in the same direction: the market is validating durable, multi-system correction for protein deficiencies. The companies that win will not be the ones with a single asset in a single disease. They will be the ones with a platform that can address the second, fifth, and fiftieth indication using the same process they used for the first.

At Glafabra, that is the thesis we are building on. Our lead program in Fabry is supported by published five-year proof-of-concept data from the investigator-initiated FACTS study conducted by our co-founders under Canadian regulatory oversight: durable therapeutic enzyme expression, a 48% reduction in toxic lyso-Gb3 from no-ERT baseline, and zero product-attributable serious adverse events. We are advancing the same platform into Pompe and Gaucher. The market is real, it is knowable, and the biology keeps suggesting it is far larger than any one drug - one disease indication.

Market figures drawn from company filings: Sanofi 2024 quarterly reports (Fabrazyme, Cerezyme, Myozyme/Lumizyme); Takeda FY2023/FY2024 results (Replagal, Vpriv); Amicus Therapeutics full-year 2024 results (Galafold). Gaucher and Pompe class sizing cross-checked against third-party market reports. Platform scope per Bley et al., Frontiers in Genetics 2023 and the IEMbase knowledgebase. Cell-penetrating delivery result: Pido-Lopez et al., Cell Reports Medicine, 2026 (PMID 42134333; DOI 10.1016/j.xcrm.2026.102803).

Register for FREE to comment or continue reading this article. Already registered? Login here.

1